Maryland businesses: Claim your $300 exemption before year-end

If your business operates in Maryland, you may be eligible for a $300 exemption under the MarylandSaves Credit program. Here’s what you need to know:

Nonprofit start-ups: Form 1023 or 1023-EZ?

When new nonprofits apply to the IRS for approval to be 501(c)(3) tax-exempt organizations, which form should they use, Form 1023 or 1023-EZ? The first is much longer and more costly to file. However, not all nonprofits qualify to use the shorter, less expensive-to-file Form 1023-EZ. Contact the nonprofit advisors at SEK for help selecting and filing a form.

Understanding GASB 101: Accounting for Compensated Absences

The Governmental Accounting Standards Board (GASB) issued Statement No. 101 (GASB 101), Compensated Absences, in June 2022. A compensated absence refers to paid leave earned by employees for time off, such as vacation leave, sick leave, holiday leave, or other types of paid time off.

Your guide to Medicare premiums and taxes

Medicare health insurance premiums can add up to big bucks — especially if you’re upper-income, married, and you and your spouse both pay premiums. Read on to understand how taxes fit in. Contact the CPAs and tax advisors at SEK with your tax questions.

What local transportation costs can your business deduct?

You and your small business likely incur a variety of local transportation costs each year. Commuting costs aren’t deductible, but the cost of any local trips you take for business purposes is a deductible business expense. Contact the CPAs and tax advisors at SEK with your tax deduction questions.

Intellectual Property Requires Careful Estate Planning

For estate planning purposes, intellectual property (IP) raises two questions: 1) what’s the IP worth and 2) how should it be transferred? You should also consider your income needs and who’s in the best position to monitor your IP rights and take advantage of their benefits. Contact the estate planning advisors at SEK for planning strategies that address IP.

Should your nonprofit compete, collaborate or both?

Not-for-profits often collaborate with other organizations with similar missions and values. But due to limited donor and grant maker resources, you also need to think about similar nonprofits as competitors. However, if a competitor has access to resources and connections you don’t (and vice versa) it may make sense to collaborate. Contact the nonprofit advisors at SEK with your financial questions.

Senior tax-saving alert: Make charitable donations from your IRA

Are you age 70½ or older and want to give to charity? You can make cash donations directly from your IRA to IRS-approved charities free of federal income tax with qualified charitable distributions (QCDs). Contact the tax advisors at SEK with questions.

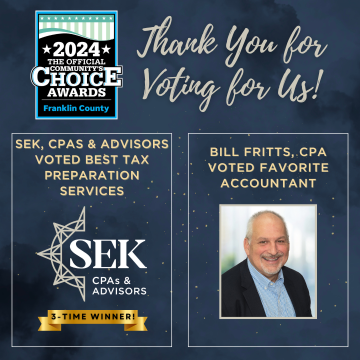

SEK named Best Tax Preparation Service in Franklin County’s Best Awards

SEK, CPAs & Advisors has been voted Best Tax Preparation Services in the Public Opinion’s Franklin County’s Best Community’s Choice Awards for 2024.

Kara Darlington elected Managing Member of SEK

SEK, CPAs & Advisors is pleased to announce the election of Kara Darlington, CPA, as the firm’s Managing Member, effective January 1, 2025.